The story of India’s car market in 2025 is one of growth, surprises, and a major mid-year twist. The industry clocked in a solid 7.71% increase in overall sales, showing clear consumer confidence. But the real story lies in the shuffle among the top five players, where market shares shifted in telling ways. A key catalyst? The landmark GST 2.0 reforms introduced in September. This policy change, which lowered taxes on smaller cars and other segments, acted like a “turbo boost,” supercharging demand in the final months of the year and reshaping the race

Rank | Manufacturer | CY25 Consumer Sales (Units) | Market Share (CY25) | Market Share (CY24) | Trend |

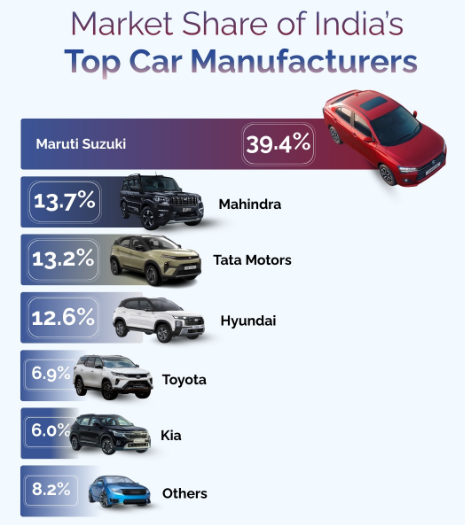

1 | Maruti Suzuki | 1,786,226 | 39.91% | 40.24% | ⬇️ Slight Dip |

2 | Mahindra & Mahindra | 592,771 | 13.25% | 12.08% | ⬆️ Strong Growth |

3 | Tata Motors | 567,607 | 12.68% | 13.18% | ⬇️ Modest Dip |

4 | Hyundai Motor India | 559,558 | 12.50% | 13.76% | ⬇️ Notable Drop |

5 | Toyota Kirloskar Motor | 320,703 | 7.17% | 6.39% | ⬆️ Steady Gain |

Maruti Suzuki: The Unshakeable King Faces Subtle Winds of Change

Maruti Suzuki’s position is like a mountain—massive and dominant. Selling over 1.78 million cars directly to consumers, it holds a market share that its closest rival doesn’t even come halfway to. The company was a production powerhouse, rolling out a record 2.25 million units in 2025.

However, the mountain experienced a slight erosion. Its market share slipped a fraction from the previous year. In a booming market, simply holding your ground means others are growing faster. This tiny dip signals that while Maruti’s mass-market appeal is unchallenged, the intense competition in high-growth segments like SUVs is starting to make its vast dominance look just a little less absolute.

Mahindra & Mahindra: The SUV Juggernaut on a Roll

If there’s one clear winner in the narrative of 2025, it’s Mahindra. The company didn’t just grow; it surged, posting the most significant market share gain among the top five. This was no accident, but a direct reward for a fiercely focused strategy. Mahindra doubled down on what it does best: building desirable, rugged SUVs.

Models like the Scorpio-N, XUV700, and the iconic Thar didn’t just sell; they often commanded long waiting lists, becoming symbols of aspiration. The company’s own data shows its SUV division had a blockbuster year, selling nearly 476,500 utility vehicles domestically and achieving its highest-ever volumes. Furthermore, Mahindra was a standout in the electric vehicle (EV) race, witnessing a staggering 369% growth in EV sales, catapulting it to third place in that high-potential segment. Mahindra’s rise is a clear sign of India’s enduring love affair with the SUV, a trend it masterfully harnessed.

Tata Motors: The EV Pioneer Navigates Crosswinds

Tata Motors presents a fascinating paradox. On one hand, it achieved its highest-ever annual sales for the fifth consecutive year, a remarkable feat of consistent growth. It sold over 81,000 electric vehicles in CY25, an 18% increase, and its Nexon was the country’s best-selling car in key months like October and November.

On the other hand, it lost its No. 2 rank to Mahindra and saw its market share shrink. Why? The explanation lies in the very segment Tata pioneered. While it remains India’s top-selling EV brand, its once-overwhelming market share in EVs has fallen to around 40%, as competitors like MG and Mahindra itself have entered the fray aggressively. So, while Tata is successfully growing the EV pie and expanding its total volume, the intensifying competition across the board is applying pressure on its overall slice of the market.

Hyundai Motor India: In Need of a Refresh

Hyundai’s story in 2025 was one of facing headwinds. It experienced the most pronounced market share decline among the leaders. While workhorses like the Creta SUV continued to perform strongly (with over 200,000 wholesale units), the overall momentum slowed.

The challenge seems to be one of an ageing portfolio in certain key categories. In a market where consumers are spoiled for choice with new features and aggressive designs from rivals, some of Hyundai’s offerings lost a bit of their freshness. The company’s growth in the EV space, though impressive at over seven times its previous year’s sales, started from a very small base and wasn’t enough to offset the broader slowdown[ciration:3]. The results suggest Hyundai is at a stage where strategic refreshes and new launches are crucial to recapture its previous growth trajectory.

Toyota Kirloskar Motor: The Steady and Strategic Climber

Toyota embodies the philosophy of slow and steady growth. With a record sales year of nearly 389,000 total units (including exports), it strengthened its position with a solid market share gain. Toyota’s success is built on a twin-pillar strategy: legendary reliability and smart partnerships.

Its own models, like the Innova HyCross and Fortuner, dominate their segments based on trust and rugged capability. Simultaneously, its deep collaboration with Maruti Suzuki—which produces models like the Urban Cruiser Hyryder and Glanza for Toyota—gives it a strong foothold in more volume-driven segments. This balanced approach, offering everything from dependable people-movers to capable SUVs, allows Toyota to grow consistently without the dramatic swings seen by some competitors.

The Road Ahead

The data from 2025 paints a clear picture: India’s car market is maturing and diversifying. The era of a single dominant trend is over. Success now comes from multiple directions: dominating the SUV craze (Mahindra), leading an electric future (Tata), offering unmatched value and network (Maruti), or building unshakeable brand trust (Toyota).

With supportive policies like GST 2.0 in place and rural demand picking up strongly, the foundation for 2026 looks positive. The battle will likely intensify further, with each automaker playing to its unique strengths in a market that rewards clear strategy as much as it does sheer volume.

Ghananand is the Founder & Chief Editor of NewzStrome. Hailing from Prayagraj, Uttar Pradesh, he brings 1.5 years of hands-on experience in journalism and digital media. He delivers sharp, unbiased, and timely news from India and across the globe. Passionate about investigative reporting, technology, politics, and lifestyle, Ghananand is committed to bringing readers nothing but the truth