India’s railway sector is going through a historic transformation, driven by record government capital expenditure, rapid electrification, and long-term infrastructure planning. Companies directly linked to Indian Railways are expected to benefit from this momentum, and Rail Vikas Nigam Limited (RVNL) is one of the most closely watched names in this space.

As investors look beyond short-term volatility, a common question arises: where could RVNL’s share price be in the next three years? While price predictions depend on multiple variables, examining the company’s fundamentals, order book strength, and growth strategy provides useful insight

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

About Rail Vikas Nigam Limited (RVNL)

Rail Vikas Nigam Limited is a Navratna public sector undertaking under the Ministry of Railways. The company primarily functions as a project execution agency, responsible for implementing key railway infrastructure projects across India.

RVNL’s core areas of work include:

Construction of new railway lines and doubling projects

Railway electrification and gauge conversion

Development of major bridges and rail infrastructure

Execution of time-sensitive and complex railway projects

The company coordinates closely with zonal railways to ensure timely completion and operational efficiency.

Key Factors Supporting RVNL’s Outlook Over the Next 3 Years

1. Strong Order Book Ensures Visibility

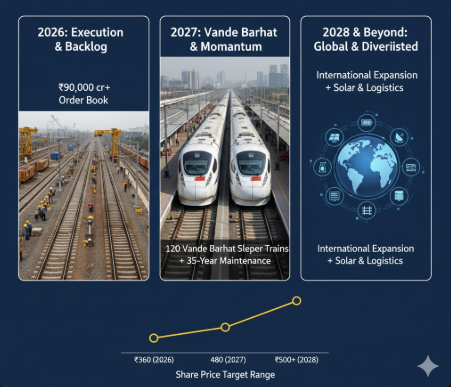

RVNL currently holds an order book of around ₹900 billion, which offers strong revenue visibility for the medium term.

Approximately ₹430 billion comes from legacy Indian Railways contracts

Around ₹460 billion comes from projects won through competitive bidding

This balance helps the company maintain execution continuity while gradually reducing dependence on direct railway nominations.

2. Expanding Beyond Core Railway Projects

RVNL has been steadily diversifying its business model. One of the most notable developments is its entry into the multimodal logistics park segment in partnership with National Highway Logistics Management.

Four logistics parks are already in different stages of implementation

These assets are expected to create long-term revenue streams

Additionally, RVNL has started bidding for Hybrid Annuity Model (HAM) projects, which provide stable and predictable income over concession periods ranging from 20 to 25 years.

3. Revenue Growth Expectations

Management estimates place annual revenue between ₹200 billion and ₹220 billion in the near term, with a target of at least 10% growth by FY27.

Growth drivers include:

New projects with shorter execution timelines

Improved project selection and faster billing cycles

Continued infrastructure spending by the government

While growth has been modest in recent years, upcoming projects could improve momentum.

4. Focus on Improving Margins

RVNL has clearly stated its intention to prioritise better-margin projects. This includes:

Selective bidding where competition is relatively low

Increased participation in HAM-based projects

Exploring overseas infrastructure opportunities that offer higher profitability

If margin discipline improves, earnings growth could outpace revenue growth.

Challenges That Could Impact RVNL

Dependence on Government Spending

A large portion of RVNL’s business is still linked to Indian Railways. Any slowdown in public infrastructure spending, delays in approvals, or changes in tendering norms could affect order inflows.

Flat Financial Performance in Recent Years

Over the last three years:

Revenue growth has remained largely flat

Profit growth has been modest, despite occasional margin improvement

This highlights the importance of execution efficiency and project mix going forward.

Sensitivity to Policy and Budget Decisions

As a PSU, RVNL’s performance is closely tied to government policies and budget allocations. Shifts in infrastructure priorities or capex allocations may influence future growth.

Financial Snapshot

RVNL Financial Highlights (₹ million):

FY23 Revenue: 202,816

FY24 Revenue: 218,785

FY25 Revenue: 199,230

Profit margins have remained in the 6–7% range, reflecting steady but unspectacular profitability.

In Q2 FY26, RVNL reported year-on-year revenue growth, but net profit declined due to cost pressures and execution-related factors.

What Lies Ahead for RVNL Over the Next Three Years?

India’s long-term railway vision, including Amrit Kaal Vision 2047, combined with continued capital expenditure of ₹2,652 billion in FY26, provides a supportive backdrop for railway-focused companies.

For RVNL, the next three years will depend on:

Execution speed and project completion

Margin improvement through selective bidding

Success of diversification into logistics and HAM projects

If these factors align, RVNL could strengthen its financial position and improve market sentiment. However, consistent performance will be crucial for sustained share price appreciation.

Conclusion

RVNL remains a strategically important player in India’s infrastructure ecosystem. While recent results have been mixed, its strong order book, diversification efforts, and government-backed projects provide long-term support.

Investors tracking RVNL share price over the next three years should closely follow execution quality, margin trends, and policy developments before making any investment decisions.

Disclaimer:

This narrative is solely intended for educational reasons. The opinions and suggestions are not those of Mint, Before making any financial decisions, we suggest investors to speak with qualified specialists. ( THIS POST IS FOR EDUCATIONAL PURPOSE ONLY)

Ghananand is the Founder & Chief Editor of NewzStrome. Hailing from Prayagraj, Uttar Pradesh, he brings 1.5 years of hands-on experience in journalism and digital media. He delivers sharp, unbiased, and timely news from India and across the globe. Passionate about investigative reporting, technology, politics, and lifestyle, Ghananand is committed to bringing readers nothing but the truth